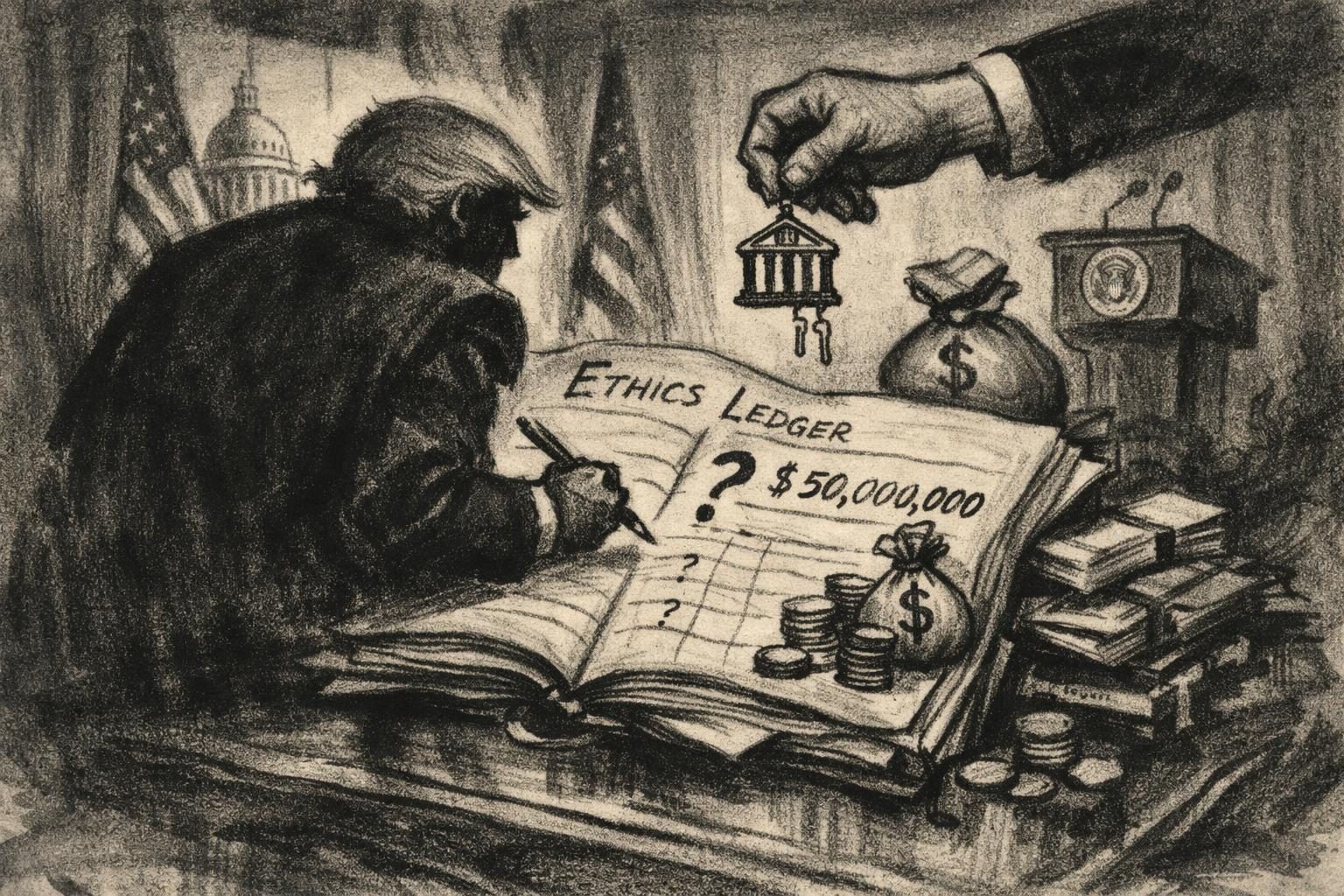

Trump’s new Schwab loan adds another weird line to the ethics ledger

Donald Trump’s latest ethics filing added a fresh and awkward item to an already crowded financial disclosure: a loan of more than $50 million from Charles Schwab in 2025. The filing, reported July 1, does not by itself establish any wrongdoing, and a loan is not inherently suspect. But in Trump’s case, nearly every personal financial move gets read through the lens of his office, his businesses, and the long-running blur between private gain and public power. The result is that even a routine-looking borrowing arrangement can feel like another test of how much daylight still exists between the president and the institutions doing business with him. The new entry sits inside a broader disclosure picture that also pointed to substantial income from crypto and other ventures, reinforcing the sense that Trump’s finances remain less a sideline than a central feature of his political identity.

The question raised by a loan like this is not simply whether it is legal, but whether it is ethically comfortable in the first place. Loans can be one of the quiet channels through which influence flows, because they do not need to resemble a cash payoff to create a public concern. A bank or financial firm that has a business relationship with a sitting president is not automatically engaged in favoritism, and there is no public evidence in the filing itself that Charles Schwab obtained anything in exchange for extending credit. Still, the overlap is hard to ignore when the borrower is also the country’s most powerful elected official. That overlap matters because presidents make decisions that can affect financial regulation, markets, taxes, enforcement priorities, and the overall climate in which major institutions operate. Even when a transaction is legitimate on paper, it can look to the public like a reminder that the office and the officeholder are never fully separable.

That discomfort is amplified by the way Trump has spent years turning his own name into a kind of political and commercial infrastructure. His brand, his campaigns, his media ecosystem, and his business interests often seem to feed one another, creating a system in which influence is rarely confined to one lane. The ethical concern is not limited to whether a single lender can be said to have crossed a line. It is the cumulative picture of a president whose personal financial life stays active, lucrative, and difficult to disentangle from his governing choices. A multimillion-dollar loan from a major financial institution may not sound as flashy as a headline-grabbing donation or a criminal allegation, but in the Trump era it lands in a more unsettling category: the ordinary transaction that becomes extraordinary because of who is involved. Critics have long argued that disclosure rules arrive too slowly and reveal too little to give the public a real-time sense of where conflicts might exist. Trump’s latest filing gives that complaint a new example to point to.

The larger political impact is likely to build gradually rather than erupt all at once. Each fresh disclosure makes it harder for the White House to present Trump’s finances as a separate matter from the presidency itself. Each line item invites another round of questions about whether policy choices are being made in a vacuum or in a world crowded with business relationships and personal incentives. And each new entry gives opponents more material to argue that the administration has normalized a standard of self-enrichment that would have been hard to imagine for previous presidents. The filing does not prove abuse, and it does not settle the broader debate over what should count as acceptable for a modern president with extensive private wealth. But it does underline the basic problem: the ethics ledger keeps growing, the entries keep getting stranger, and the public keeps being asked to treat those disclosures as normal when they plainly do not feel normal at all. That is how a single loan becomes part of a much bigger story about power, money, and the worn-out guardrails meant to keep them apart.

Comments

Threaded replies, voting, and reports are live. New users still go through screening on their first approved comments.

Log in to comment

No comments yet. Be the first reasonably on-topic person here.